The Shift

For the last three years, the American stock market has been defined by a single, overwhelming theme, size.

If you invested in the largest technology companies, the "Magnificent Seven," you likely saw significant returns. These giants benefited from the artificial intelligence boom, immense cash reserves, and a widespread belief that in an uncertain economy, bigger was safer.

Conversely, if you invested in the smaller companies that make up the backbone of the domestic economy, you were largely left behind. High interest rates punished them, and their stock prices stagnated.

Now, in the first two weeks of 2026, the market’s leadership has abruptly changed.

Since New Year's Day, the Russell 2000, the benchmark index for small publicly traded companies, has surged nearly 6 percent, significantly outpacing the S&P 500. On Wall Street, this phenomenon is being called "The Great Rotation."

The theory driving this shift is straightforward:

- The Federal Reserve has begun cutting interest rates, lowering the cost of doing business.

- The economy is growing at a robust 5.3 percent pace, defying fears of a recession. 3

- The recently passed "American Competitiveness Act" has introduced new tax incentives designed to favor American manufacturers over global conglomerates.

On the surface, the environment seems perfect for smaller companies to catch up.

The Complication

However, a deeper look at the data reveals a significant structural flaw in this rally. The small-company universe is currently divided into two distinct groups, and the market is currently lifting both of them indiscriminately.

- The Builders: These are profitable industrial firms and manufacturers. They are generating cash and utilizing the new tax credits to expand factories and upgrade fleets.

- The Borrowers: This is a large cohort of companies—roughly 43 percent of the index—that do not currently generate a profit. They rely heavily on debt to fund their daily operations.

For much of the last decade, the second group survived because borrowing costs were historically low. That era has ended, and a financial deadline is approaching.

The Maturity Wall

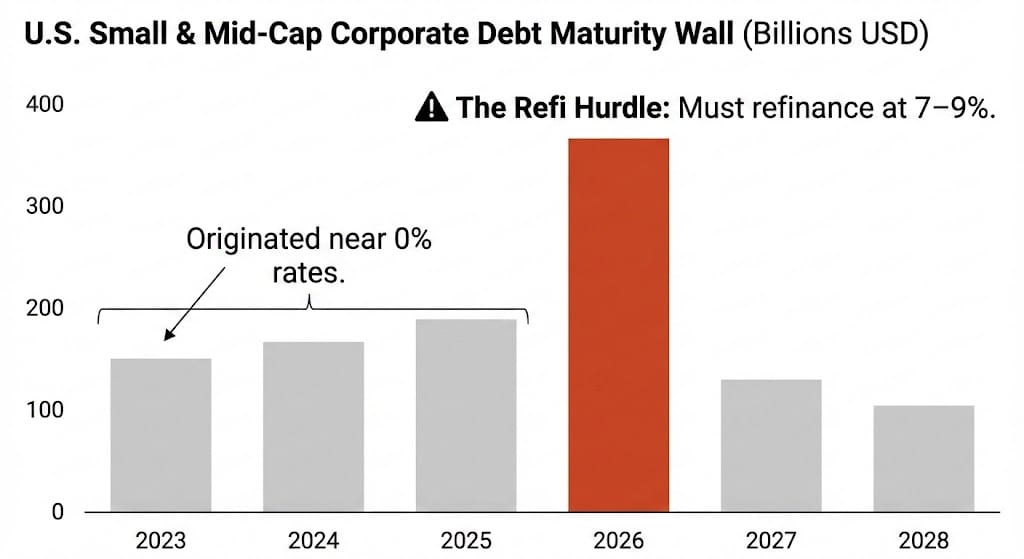

To understand the risk, it helps to look at the corporate calendar.

In 2026, small and mid-sized U.S. companies must refinance approximately $368 billion in debt. Even with the Federal Reserve’s recent rate cuts, the math for these companies is difficult.

Many of these loans were originated in 2020 and 2021, when interest rates were near zero. As these loans come due this year, companies will be forced to refinance them at current market rates, which remain significantly higher. Lenders, wary of credit risk, are presently demanding interest rates between 7 and 9 percent for smaller borrowers.

Unlike a giant like Apple, which uses long-term fixed bonds to lock in low rates, smaller companies often rely on floating-rate debt. This means their interest payments rise almost immediately when rates tick up or credit conditions tighten. For a company operating with thin profit margins, a doubling of interest expenses is not merely a financial headwind; it is a threat to solvency.

Quality Wins

The optimistic case remains valid for specific businesses. The new tax law’s 100% bonus depreciation rule, which allows companies to immediately deduct the cost of new equipment, is a substantial benefit for profitable industrial firms. Companies like Comfort Systems USA (FIX) or Argan, Inc. (AGX), which fund their own growth through profits rather than debt, are well-positioned to thrive.

The rotation into small stocks is based on real economic changes, but it carries a hidden danger for passive investors. The "rising tide" of the economy will not lift every vessel. The prudent strategy is to distinguish between the companies with healthy balance sheets (often found in the S&P 600 index, which requires profitability for inclusion) and the broader, debt-laden index.

Latest News

TSMC (TSM)

- The world's largest chipmaker raised its capital expenditure guidance to over $50 billion.

- This is fuel for the small-cap supply chain. Equipment makers like Onto Innovation (ONTO) and MKS Instruments (MKSI) rallied in kind.

- The trade has moved from "buying the chips" to "buying the machines that make the chips."

Talen Energy (TLN)

-

The independent power producer announced a $3.45 billion deal to acquire natural gas assets in the PJM grid (Ohio/Indiana).

-

This is an "AI Infrastructure" play. Data centers need constant, reliable power that wind and solar cannot yet provide alone.

-

Talen is effectively cornering the market on the "dispatchable electrons" needed by Amazon and Microsoft.

Biotech

-

Beam Therapeutics (BEAM) The biotech firm rose 20% after the FDA agreed to an "accelerated approval path" for its gene-editing therapy.

-

On the flip side, Arcus Biosciences (RCUS) crashed after a failed Phase 3 cancer trial. The divergence highlights the binary nature of the sector: regulatory wins create massive alpha, while clinical failures wipe out value overnight.

Movers & Shakers

- Bank OZK (OZK) Up 6.2% The mid-cap lender rallied following the positive news from First Horizon (as covered yesterday). Investors are betting that a stable economy will restart paused construction projects in the South, where the bank is heavily exposed.

- Kulicke and Soffa (KLIC) Up 8.4% Shares of the equipment maker rose on the heels of the strong report from TSMC. The company builds the specialized tools needed to package advanced AI chips, positioning it to benefit directly from the industry's spending boom.

- Applied Digital (APLD) Up 11.5% The data center operator jumped after securing a $300 million loan to expand its campus in North Dakota. It is the latest sign that smaller, agile companies are racing to build the physical infrastructure for AI—sometimes faster than the tech giants can.

- Sterling Infrastructure (STRL) Up 5.5% The mid-sized construction firm hit a new high. Sterling specializes in preparing the ground for massive projects—from data centers to highways. As companies like Amazon and Google break ground on new facilities, Sterling is often the first phone call they make.

The Briefing

The Economy

- Strong Growth: The Atlanta Fed’s latest model forecasts GDP growth of 5.3 percent for the fourth quarter. This data suggests the economy is re-accelerating rather than slowing down, challenging the "soft landing" narrative.

- The Fed's Dilemma: Because growth is so robust, traders are beginning to expect the Federal Reserve to pause its rate-cutting campaign later this month. Central bankers remain wary of lowering rates too quickly, lest inflation reignite.

The Markets

- Housing Resilience: Despite mortgage rates remaining elevated, homebuilder stocks (tracked by the ETF ITB) have risen 13 percent this year. A persistent shortage of existing homes for sale has effectively forced buyers into the new-construction market.

- Banking Risks: Regional bank stocks have stabilized, but they face a challenge. Approximately $1.5 trillion in Commercial Real Estate loans will mature this year. As banks preserve capital to cover potential losses in office real estate, they are tightening lending standards for small businesses.

The Policy

- Consumer Stimulus: The provision in the new tax law eliminating federal taxes on tips and overtime pay is now in effect. Economists expect this to boost disposable income for service workers, potentially benefiting casual dining chains and regional retailers.

The Flows

- Moving Money: In the first week of January, investors withdrew $4.6 billion from large-cap funds and moved $267 million into small-cap value funds. This indicates that professional asset allocators are actively repositioning their portfolios for a broader market rally.

Today's Fact

On January 16, 1919—107 years ago today—the United States ratified the 18th Amendment, effectively banning the sale of alcohol and ushering in the Prohibition era.

While the law destroyed the legal brewing industry (wiping out thousands of small businesses), it inadvertently created one of the most lucrative "black markets" in history. The bootlegging industry grew so large that by the mid-1920s, the "shadow economy" of illegal alcohol was estimated to be worth $3 billion annually, roughly equivalent to $55 billion today.

The Investment Lesson: Government regulation never truly kills demand; it simply displaces it. In 2026, we see the same dynamic in the AI chip market, where US export bans to China have created a thriving "gray market" for processors, boosting sales for third-party distributors in Asia.

Thank you for your time this morning. Have a great weekend, I'll be back Monday with another edition. -Marques

Sign up here to get this newsletter in your inbox. Reach our team at marques@blankcapitalresearch.com

|

From the Desk of Marques Blank I write this newsletter from my desk in Chanhassen, MN, usually with a strong coffee in hand. My goal is simple: To provide you the news you need to know in the small and mid-cap world. I sort through the filings so you don't have to. |